open Thursday")

Report Overview

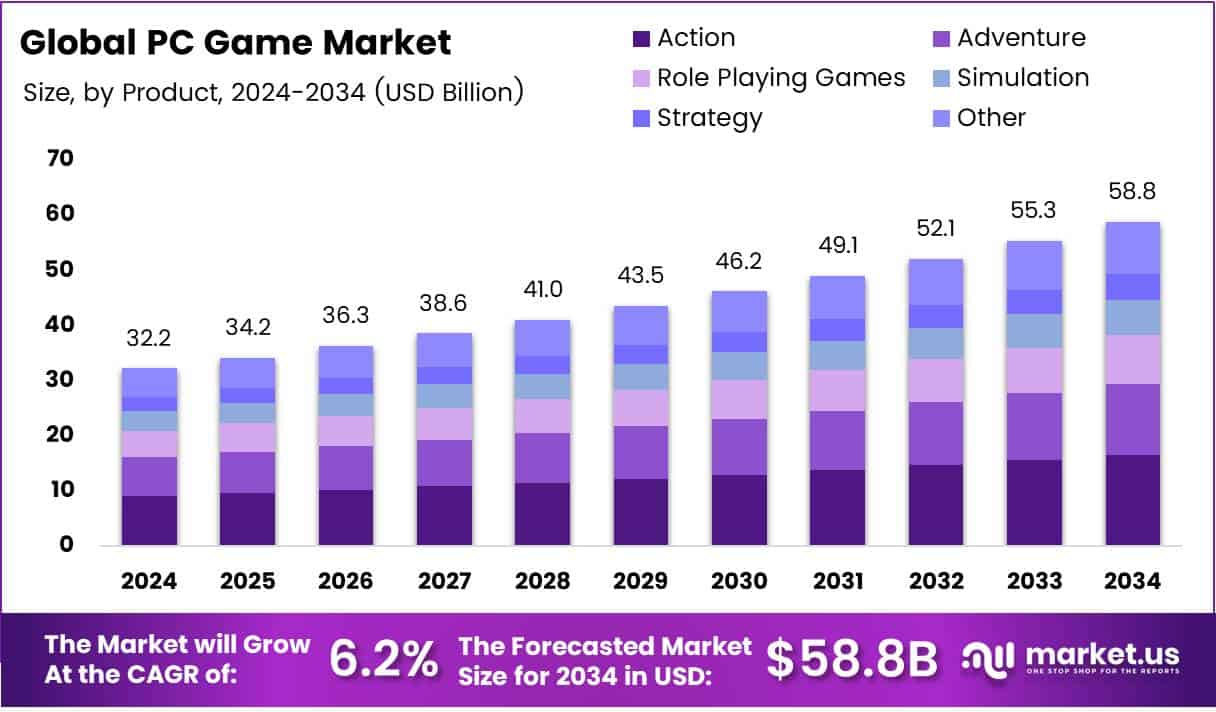

The Global PC Game Market size is expected to be worth around USD 58.8 Billion by 2034, from USD 32.2 Billion in 2024, growing at a CAGR of 6.2% during the forecast period from 2025 to 2034.

The PC game market represents a dynamic and ever-evolving segment within the global gaming industry, driven by the rapid advancements in technology and an expanding gamer demographic. According to Prioridata, PC remains the leading platform for game development, with 63% of game developers creating content specifically for PC.

The platform is favored by gamers for its high customization potential, superior graphics capabilities, and access to a wide variety of game genres. As of 2024, there are approximately 3.3 billion active video gamers worldwide, a number expected to exceed 3.5 billion by 2025. This significant expansion highlights the growing importance of PC gaming as a central player in the global gaming ecosystem.

The PC game market is also being shaped by the surge in interest for game-as-a-service (GaaS) models, with Exploding Topics reporting that in 2024, 1.8 billion gamers opted for low-end GaaS PC gaming, a rise of 800 million compared to 2008.

This shift reflects how digital game distribution, continuous updates, and online multiplayer experiences are becoming increasingly attractive to a wide range of gamers, especially in emerging markets. As the number of players continues to grow, the PC gaming industry is presented with immense potential for revenue generation and market expansion.

The growth trajectory of the PC game market is particularly promising, with substantial opportunities in both emerging and mature markets. A major driver for this growth is the increasing accessibility of gaming hardware and internet infrastructure, enabling players from diverse economic backgrounds to access high-quality gaming experiences.

Government investments in technology and innovation are further accelerating this trend, with several countries recognizing the potential economic benefits of a booming gaming industry. Governments are offering funding and incentives to developers, fostering a more competitive and innovative environment in which the market can thrive.

The regulatory landscape surrounding PC games is also evolving, with new policies focused on digital gaming safety, data protection, and fair play. These regulations aim to create a secure and equitable gaming environment for players, which, in turn, boosts consumer confidence.

Governments are also addressing issues like microtransactions and loot boxes, which have sparked significant debate among gamers and regulators alike. With steady investments from both the private and public sectors, and a favorable regulatory environment, the PC game market is poised for robust growth, attracting new investors and stakeholders from around the globe.

Key Takeaways

- Global PC game market projected to reach USD 58.8 Billion by 2034, growing at a CAGR of 6.2% from 2025 to 2034.

- Action games lead the market with a 32.4% share in the By Type of Genre Analysis segment in 2024.

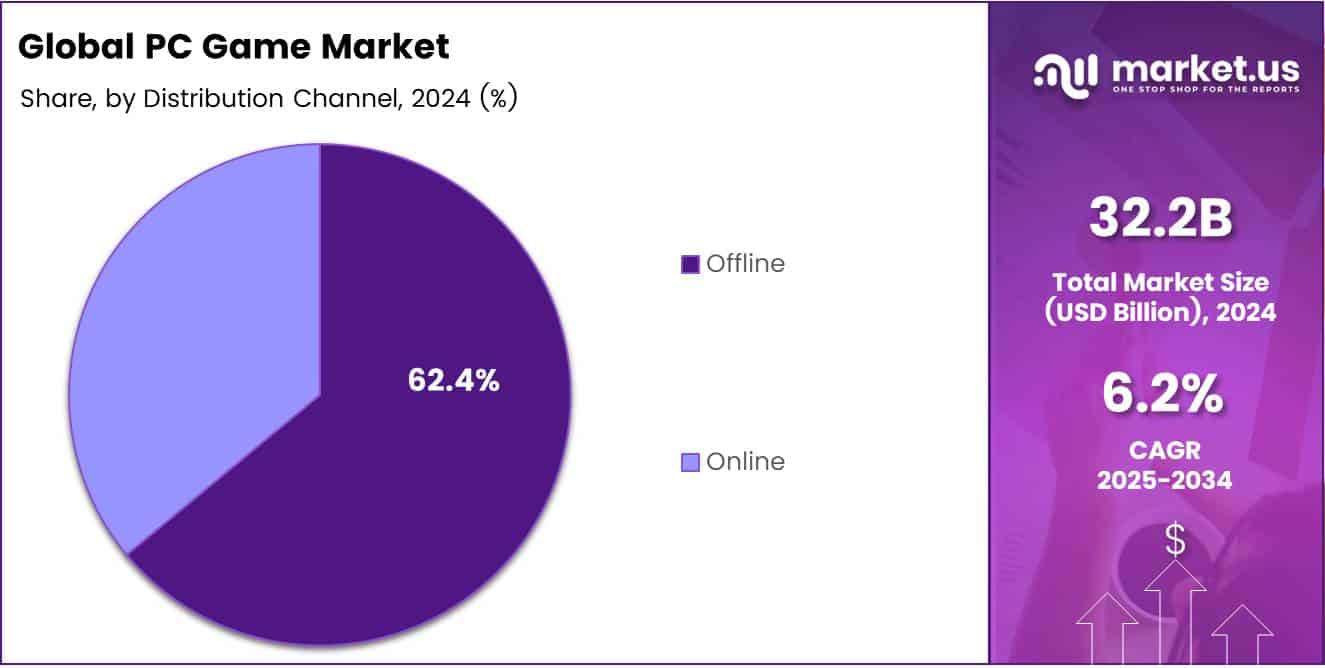

- Offline distribution channel holds a dominant 62.4% share of the market in 2024, driven by the popularity of physical game copies.

- North America remains the largest region, with a 33.2% market share, valued at USD 10.6 Billion in 2024.

Type of Genre Analysis

Action Games Lead PC Game Market with 32.4% Share in 2024, Driven by Popularity and Engagement

In 2024, Action games maintained a dominant position in the PC game market, capturing a 32.4% share within the By Type of Genre Analysis segment. This strong market presence can be attributed to their widespread popularity, immersive gameplay experiences, and continuous innovations that attract a large, diverse player base. Action games remain a favorite among PC gamers due to their dynamic environments and engaging mechanics, keeping players hooked with ever-evolving storylines and multiplayer capabilities.

Following Action, Adventure games held a significant portion of the market, appealing to players with their rich narratives and explorative gameplay. Meanwhile, Role Playing Games (RPGs) attracted a loyal following through their deep storytelling, character development, and strategic complexity.

Simulation games also gained traction, with their focus on real-world experiences and virtual reality advancements, offering players a lifelike experience. Strategy games continue to resonate with a niche audience, valuing tactical thinking and long-term planning.

The Other Games category encompasses a wide variety of subgenres, contributing to the diverse nature of the PC gaming ecosystem. Together, these genres illustrate the evolving landscape of PC gaming and the shifting preferences of players worldwide.

Offline Distribution Channel

Offline Distribution Channel Leads the PC Game Market with 62.4% Share in 2024

In 2024, the Offline distribution channel maintained a dominant position in the PC game market, commanding an impressive 62.4% market share. This trend can be attributed to the continued popularity of physical game copies, especially in regions where internet access may be limited or consumers prefer tangible products.

Offline distribution channels, including brick-and-mortar retail stores, have a long-standing relationship with gamers who enjoy the immediate access to physical games, as well as the experience of browsing and purchasing in-store. Furthermore, in many countries, offline retail remains the preferred method for acquiring high-end gaming products, including collector’s editions and special releases.

In contrast, the Online distribution channel, while growing in prominence, accounted for a smaller portion of the market, driven by the rise of digital platforms like Steam and Epic Games Store. Online sales are especially popular in regions with high-speed internet access, offering the convenience of direct downloads and often lower prices.

However, despite its growing adoption, the Online segment still lags behind offline retail in terms of overall market share. As digital downloads continue to evolve and internet infrastructure improves, the Online channel is expected to see a steady increase in market share in the coming years.

Key Market Segments

By Type of Genre

- Action

- Adventure

- Role Playing Games

- Simulation

- Strategy

- Other Games

By Distribution Channel

Drivers

Advancements in Technology Boost the PC Game Market

The continuous advancements in PC hardware, particularly in components like GPUs, CPUs, and RAM, have significantly improved the overall gaming experience. These technological upgrades allow for more visually stunning and high-performance games, attracting both casual and hardcore gamers.

As hardware becomes more powerful, game developers can push the boundaries of graphics, gameplay, and virtual environments, offering players increasingly immersive and realistic experiences. This, in turn, drives demand for PC games, as players seek to leverage the capabilities of the latest systems.

The constant innovation in gaming technology creates a dynamic market where new titles can thrive, appealing to gamers who want to experience cutting-edge graphics and smoother gameplay. Moreover, this progress fuels the creation of more complex and expansive game worlds, ensuring that gamers continue to invest in high-performance PCs.

As technology advances, the PC game market is poised for continuous growth, with both players and developers benefiting from the ever-improving hardware ecosystem.

Restraints

High Initial Cost of Gaming PCs Hampers Market Growth

One of the key restraints in the PC game market is the high initial cost associated with building or purchasing a high-performance gaming PC. For many potential gamers, especially those who are on a budget, the steep prices of gaming hardware such as high-end graphics cards, processors, and monitors can be a significant barrier.

These upfront costs can deter a large segment of potential buyers from entering the market, limiting the overall growth of the gaming community. As technology continues to evolve, the demand for even more powerful machines to support the latest games and virtual experiences grows, which in turn increases the financial burden for consumers. This situation often leads some gamers to consider alternative options, such as console gaming or cloud-based gaming services, which offer lower entry costs.

Growth Factors

Rising Adoption of VR and AR Technologies Presents Major Growth for the PC Game Market

The integration of Virtual Reality (VR) and Augmented Reality (AR) into PC gaming offers exciting opportunities for market growth. As these technologies continue to advance, they create immersive experiences that make gaming more interactive and engaging, which attracts a larger, more diverse audience.

VR and AR can transport players into entirely new worlds, offering a level of immersion that traditional gaming setups cannot match. This trend could drive a shift in the types of games being developed, with a focus on more immersive, story-driven content. Additionally, the rise of cloud gaming services like Google Stadia and NVIDIA GeForce NOW is enabling gamers to enjoy high-quality titles without the need for expensive gaming hardware, making games more accessible and appealing to a broader audience.

Moreover, subscription-based services such as Xbox Game Pass for PC and EA Play are becoming increasingly popular, offering gamers access to a wide variety of games for a fixed monthly fee. This not only provides gamers with more choice but also creates a consistent revenue stream for developers and service providers. With these advancements in technology and services, the PC game market is poised for substantial growth in the coming years, driven by the demand for more immersive experiences and flexible gaming options.

Emerging Trends

Streaming and Let’s Play Content Drive PC Game Popularity

In the rapidly growing PC gaming market, streaming and Let’s Play content have become major influencers. Platforms like Twitch and YouTube Gaming are where millions of gamers showcase their gameplay and engage with audiences. This trend has significantly increased the visibility of PC games, as popular streamers and content creators introduce new titles to their fanbase. This exposure often leads to spikes in game sales and a larger player base.

Additionally, many players enjoy watching others play games before deciding to purchase, creating a strong connection between streaming content and gaming trends. Coupled with this, the increasing interest in open-world and sandbox games has fueled the demand for interactive environments where players can explore and engage in free-form gameplay. Titles with expansive worlds and high levels of player freedom, like Minecraft or Grand Theft Auto, have seen great success.

Moreover, the Game-as-a-Service (GaaS) model is becoming more common, as developers focus on live-service games that are constantly updated with new content, expansions, and in-game purchases. This model keeps players engaged for longer periods and generates consistent revenue.

Regional Analysis

North America leads with 33.2% market share valued at USD 10.6 billion driven by strong gaming culture and infrastructure

North America remains the dominant region in the global PC game market, accounting for 33.2% of the market share, valued at USD 10.6 billion. This region benefits from a robust gaming culture, significant disposable income, and a well-developed infrastructure that supports both casual and competitive gaming. The United States, in particular, serves as a key market, with its large base of gamers and home to several major game publishers and developers.

Regional Mentions:

Asia Pacific is the fastest-growing region in the PC game market, driven by a massive gamer base, particularly in countries like China, Japan, South Korea, and India. The region’s growth is fueled by the increasing adoption of gaming smartphones, affordable internet access, and the rise of esports, which has become a major cultural phenomenon. Asia Pacific’s dominance in mobile gaming also spills over into the PC game market, with younger generations increasingly adopting gaming as a mainstream form of entertainment.

Europe plays a crucial role in the PC game market, with key players such as Germany, the United Kingdom, and France leading the way. The region has a diverse gaming community, with strong support for both PC and console gaming. European gamers are increasingly adopting high-performance PCs, and the region is also home to some of the largest gaming expos, such as Gamescom in Germany, further driving market growth.

Latin America has witnessed consistent growth in the PC gaming sector, with Brazil leading the charge as the largest market in the region. The rise of the middle class and increasing internet penetration have allowed more individuals to access gaming platforms. As a result, Latin American countries have seen an uptick in both casual and competitive gaming. Mexico and Argentina also show substantial growth in the number of gamers, supported by a youthful demographic that actively engages in online gaming and esports.

Middle East & Africa (MEA) is a developing region in the PC game market, with countries like Saudi Arabia, the United Arab Emirates, and South Africa investing heavily in gaming infrastructure and esports. Saudi Arabia, in particular, is positioning itself as a future hub for gaming, with substantial investments aimed at fostering a vibrant gaming ecosystem. The UAE has also seen a rise in gaming cafes and a growing interest in competitive gaming, reflecting broader regional interest.

Key Regions and Countries

- North America

- Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

- Latin America

- Brazil

- Mexico

- Rest of Latin America

- Middle East & Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of MEA

Key Players Analysis

In 2024, the global PC game market is shaped by several industry giants whose influence continues to drive both innovation and competition. Key players such as Electronic Arts (EA) and Activision Blizzard maintain a dominant presence through their vast portfolios, ranging from sports simulators like EA Sports to expansive multiplayer franchises like Call of Duty and World of Warcraft. EA’s recurring success with live-service models and microtransactions in titles such as FIFA and Apex Legends positions them as a leading revenue generator in the market.

Ubisoft Entertainment, known for its open-world franchises such as Assassin’s Creed and Far Cry, also remains a key player, diversifying its offerings across both single-player and multiplayer genres. Their stronghold in both PC and cross-platform games is poised for continued growth, particularly in the competitive esports space.

Epic Games is increasingly shaping the market with its dominant engine, Unreal Engine, and its cultural phenomenon, Fortnite. Their continued development of Epic Games Store, along with their push into metaverse-related experiences, has given them a significant foothold in the digital distribution space.

Meanwhile, Square Enix, Bandai Namco, and Sega continue to attract loyal fan bases with both original IPs and adaptations of popular franchises. Square Enix, with its deep storytelling and RPGs like Final Fantasy, and Bandai Namco with its extensive fighting game lineup, remain pivotal in cultivating niche yet lucrative markets.

Overall, these companies, through strategic expansions, cross-platform endeavors, and engagement with emerging trends like esports and cloud gaming, will maintain a substantial influence in the evolving PC gaming market.

Top Key Players in the Market

- Electronic Arts

- Activision Blizzard, Inc.

- Ubisoft Entertainment SA

- Epic Games, Inc.

- Square Enix Holdings Co., Ltd.

- Bandai Namco Entertainment, Inc.

- Sega Inc.

- Blizzard Entertainment, Inc.

- Focus Entertainment

- 2K Games

Recent Developments

- In March 2025, Pragma raised $12.75M to develop its backend game engine aimed at enhancing live services games. This funding willa help the company further innovate in delivering scalable multiplayer experiences for online games.

- In January 2025, Morgan Stanley upgraded NetEase due to the company’s robust PC game pipeline. The upgrade reflects strong growth prospects driven by new game releases and market expansion.

- In November 2024, SayGames announced plans to invest $30M in promising mobile game projects. This strategic investment aims to support the development of innovative and high-potential mobile gaming titles.

- In May 2024, Hasbro revealed a $1 billion investment to bring video game development in-house. This move allows Hasbro to create and manage its own gaming franchises, enhancing its presence in the interactive entertainment space.

")

open Thursday")

{kind=link}